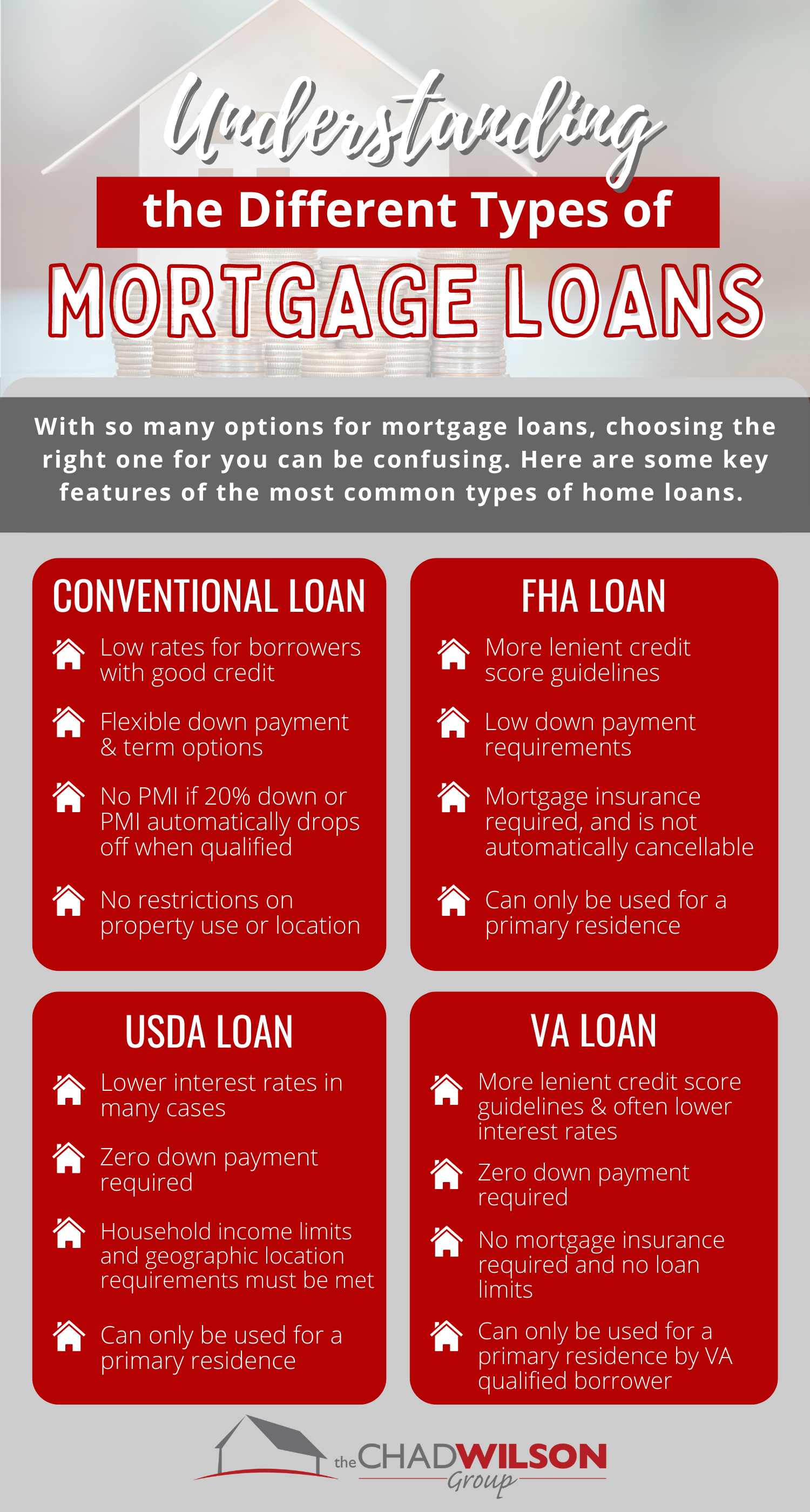

Old-fashioned Loans That have Collection Account Recommendations is followed and place by the Federal national mortgage association and you may Freddie Mac computer. FHA is considered the most prominent loan program in the united states. Most buyers off belongings think that just because he has the stuff and you will charged-of profile they could only qualify for FHA mortgage brokers and you can maybe not Old-fashioned Money. There are numerous times in which customers can also be qualify for conventional finance However FHA Financing. For example, FHA does not allow Earnings-Built Payment (IBR) on student education loans. not, IBR Money are allowed having Traditional Loans. There are more products in which homeowners can be come upon in which they do maybe not be eligible for FHA Money but tend to qualify for Old-fashioned Fund.

The us Institution from Housing and Urban Creativity (HUD) is the mother or father of one’s Federal Casing Government (FHA). FHA provides the really lenient financing recommendations regarding outstanding selections and you will billed-out-of membership. HUD 4000.1 FHA Manual sets the new credit guidelines over FHA Fund. Both Fannie mae and you may HUD enjoys separate credit advice pertaining to an excellent collection account and you may fees-away from accounts. Antique Finance which have Collection Membership Guidance was influenced by the Fannie mae and you will Freddie Mac computer. Unpaid the range membership and you will charge-of accounts are tougher having Federal national mortgage association and Freddie Mac so you can score a keen agree/eligible per Automated Underwriting Program Recognition.

Conventional Assistance Towards Series And you can Derogatory Borrowing from the bank

In this site article, we will be revealing non-mortgage traditional money with range profile guidance. Federal national mortgage association and you may Freddie Mac could be the a couple of home loan monsters that set Recommendations toward conventional fund. Lower than Federal national mortgage association Advice, overdue borrowing from the bank accounts aren’t greeting. All an excellent energetic past-due levels into customer’s credit report have to be lead newest and up up to now. The borrowing tradelines which are not reported just like the range account, should be introduced newest. Delinquent and you can delinquent accounts need to be raised to time. Which have owner-renter conventional financing having range levels, individuals commonly needed to pay a great collection levels and you may/otherwise low-financial charge off account regardless of the an excellent equilibrium. Borrowers of 2 to 4-unit owner renter residential property a great selections and charged-regarding account don’t need to be distributed whether your number is lower than $5,000. If the an excellent stuff and you may/otherwise non-mortgage recharged-off accounts was more than $5,000 on the 2 to 4-device holder-filled properties, compliant recommendations condition it should be paid in complete. The above conventional mortgage advice apply for next home financing because the well.

Money spent, Old-fashioned Mortgage Assistance

To have homebuyers whom wish in the to shop for and being qualified for a financial investment domestic, the second guidelines apply to conforming fund. Delinquent the collection membership that have a great equilibrium that’s higher than just $250 should be paid back. This new a good non-financial, charge-off accounts one equivalent or perhaps is higher than $250 and you will all in all, more than $step one,000 should be found.

HUD, the brand new mother from FHA, differs from the guidelines into a fantastic range profile. FHA classifies range membership to the around three classes:

- Scientific Collection Levels

- Non-Medical Range Account

- Charge off Membership

FHA exempts scientific collection profile and you may recharged-away from account off financial obligation to help you income proportion calculations. Information on how FHA states into-medical range levels which have outstanding balance of greater than $2,000. A good 5% off a fantastic harmony should be used as the a monthly hypothetical financial obligation. Any non-medical collection account over $2,000 will not need to be distributed. Although not, 5% of your outstanding range equilibrium is used just like the a great hypothetical loans to calculate obligations in order to income percentages of your own debtor. This won’t apply at conforming finance.

Overlays On the Traditional Loans

Over 75% your borrowers on Gustan Cho Partners Financial Classification is men who cannot be considered within most other lenders employing lender overlays. Really banking companies and you may loan providers possess her financial overlays. Even when individuals satisfy Antique Financing Assistance plus don’t has to pay outstanding series and you can/otherwise energized-out-of, loan providers need it section of their overlays. Extremely loan providers would not want to manage individuals with a good range levels and/or charge-off membership unless of course this has been paid in full and you can shown on the credit history. Loan providers do not need to honor home loan guidelines and can have higher credit conditions. Loan providers need meet minimal home loan recommendations. But not, they’re able to enjoys highest conditions titled financial overlays.

Faqs (FAQs)

step 1. What exactly are Range Account? Range profile are debts transported on the amazing creditor so you can an effective range institution on account of hit a brick wall fee. This type of account are stated on your own credit report and certainly will rather effect your credit rating. dos. Manage Range Profile Apply at My Power to Get a conventional Financing? Range accounts can impact your ability so you can be eligible for a traditional mortgage. Lenders determine your current creditworthiness, and achieving range membership may raise concerns about debt accuracy. 3. Exactly what are the Direction for Range Levels into the Old-fashioned Loans? Direction will vary by the bank, but traditional mortgage recommendations do not require consumers to repay a great collection account so you’re able to meet the requirements. not, assume the full balance off low-scientific stuff exceeds a particular tolerance (normally $dos,000). If so, particular loan providers may require commission or satisfactory agreements ahead of acceptance. 4. How can Scientific Collection Levels Feeling Conventional Mortgage Recognition? Scientific range levels are often handled a lot more leniently than other versions away from collections. Of several lenders not one of them medical series getting repaid as a disorder getting financing recognition, taking you to definitely scientific debt shall be unavoidable and unstable. 5. Do i need to Get a normal Mortgage Basically Have Current Range Accounts? Qualifying getting a normal mortgage having previous collection profile is achievable but could be much more tricky. Loan providers often take into account the age, dimensions, and kind of your own range accounts, plus complete credit reputation and you will monetary balance. 6. Must i Pay Range Accounts Before applying having a traditional Financing? While it is never requisite, paying down otherwise resolving range account is change your credit rating and you will improve your application for the loan. They reveals monetary responsibility and you can reduces the risk recognized from the loan providers. eight. How do Costs-Offs Range from Range Profile? A charge-of happens when a creditor writes off of the loans due to the fact a losses immediately following a long ages of non-fee, if you find yourself a collection membership happens when the debt is actually endorsed in order to a portfolio service. Both can also be negatively effect your own borrowing, but lenders may glance at them in another way according to the guidelines. 8. What procedures can i take to boost my likelihood of protecting a traditional loan despite collection membership? To evolve your chances: Pay-off otherwise settle the collection profile. Take care of a steady income and you can a job history. Boost your credit history because of the dealing with other costs responsibly. Save getting increased downpayment to minimize the fresh lender’s chance. 9. Were there Choices so you can Conventional Finance Basically Enjoys Collection Accounts? Solutions occur, particularly FHA finance, with a lot more lenient borrowing from the bank conditions and may become more forgiving out of collection levels. Trying information off a home loan elite can assist you in the examining every possibilities tailored towards the financial predicament.